Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Northwest Arkansas Real Estate Market Update: 2025 vs. 2024

A Year of Stability, Strength, and Smart Opportunity

Northwest Arkansas closed out 2025 exactly how strong markets do—quietly resilient. While national real estate headlines leaned into uncertainty, our local market delivered something far more valuable: steady pricing, consistent demand, and improved efficiency.

This wasn’t a year of frenzy. It was a year of fundamentals. And that’s good news as we head into 2026.

Let’s break down what actually happened in the Northwest Arkansas real estate market—and why it matters.

Home Prices Continued to Rise—Without the Chaos

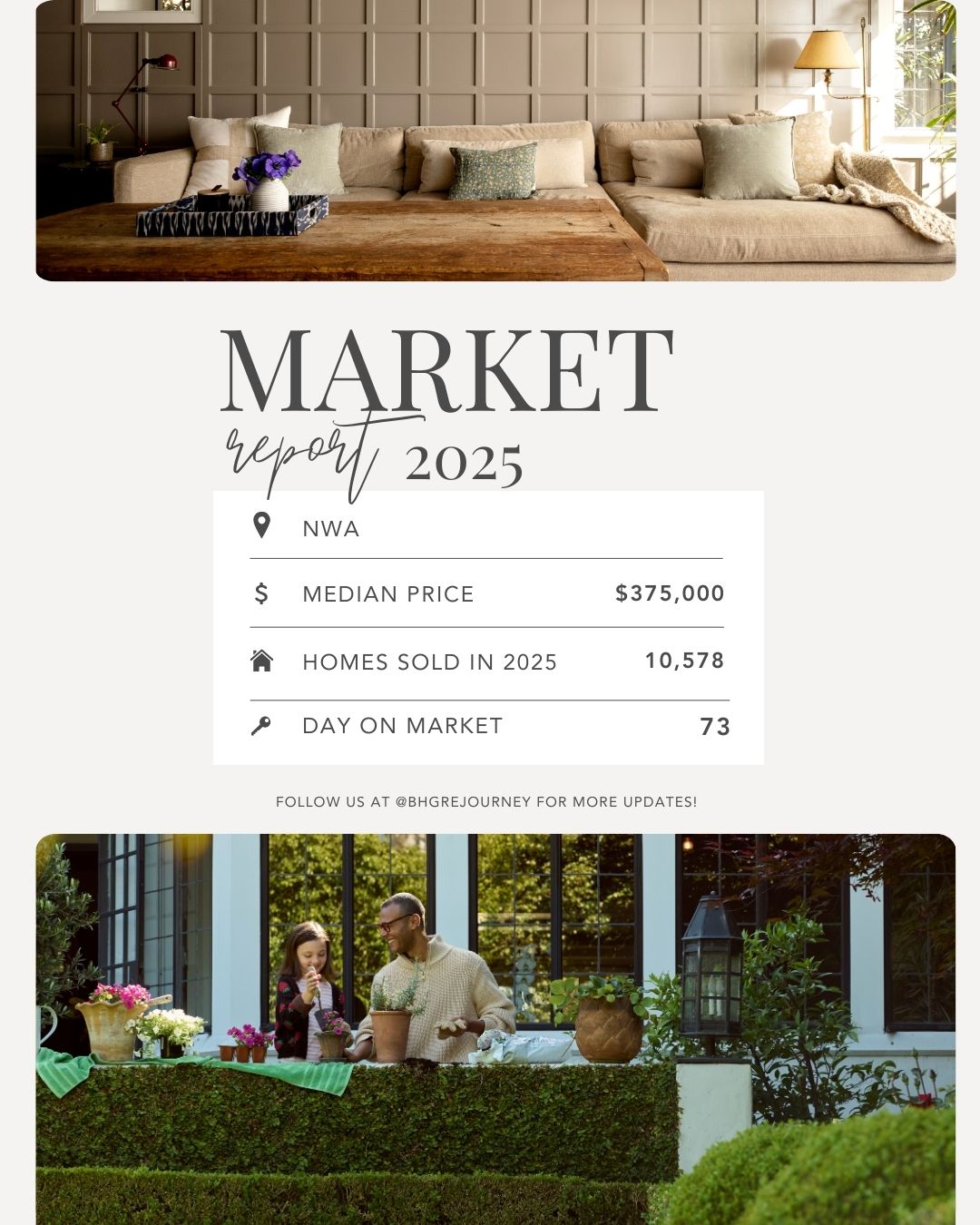

The median home price in Northwest Arkansas reached $375,000 in 2025, a 4.5% increase year-over-year from $359,000 in 2024. Since 2023, prices are up 7.76%, reinforcing a key reality: home values are still appreciating, just at a healthier, more sustainable pace.

The median price per square foot climbed to $209, also up 4.5%. That matters because it signals appreciation across the market—not just at the top end.

What this tells us:

This is no longer an overheated seller’s market—but it is far from weak. Buyers are more discerning, sellers must price strategically, and homes that are positioned well continue to perform.

Sales Volume Stayed Strong in a High-Rate Environment

One of the biggest wins of 2025? Stability.

A total of 10,578 homes sold, essentially flat compared to 2024 and up 7.8% from 2023. In a year shaped by elevated mortgage rates, holding volume steady is not accidental—it’s a signal of underlying demand.

Buyers didn’t leave the market.

They simply became more intentional.

Homes Sold Faster Than in 2024

Here’s a stat that deserves more attention:

Days on Market dropped to 73 days, an 18-day improvement year-over-year.

That means well-priced, well-presented homes moved faster in 2025—even with higher borrowing costs.

Translation for sellers: strategy matters more than ever. Pricing, presentation, and local expertise aren’t optional—they’re the difference between sitting and selling.

Mortgage Rates: The Shift That’s Setting Up 2026

Interest rates have been the headline act for the past two years. In 2025, the average mortgage rate hovered around 6.6%, down from prior peaks. More importantly, forecasts point toward rates drifting closer to 6%.

That shift is meaningful.

On a $400,000 loan, the difference between 6.6% and 6.0% is roughly $156 per month—real money that brings more buyers off the sidelines and restores confidence.

Looking Ahead: Why 2026 Is Quietly Promising

As we move into 2026, the outlook for the Northwest Arkansas housing market is constructive, balanced, and opportunity-rich.

Here’s what we’re watching:

-

More inventory entering the market as seller confidence returns

-

More buyers re-engaging as rates dip below 6%

-

Mortgage rates likely stabilizing between 5.7%–6.0% for much of the year

-

No dramatic drops—but enough movement to improve affordability and momentum

This is shaping up to be a market that rewards strategy over speculation—great for buyers who want options, sellers who price with intention, and builders planning for sustained demand rather than short-term spikes.

The Bottom Line

Northwest Arkansas continues to stand out as one of the most durable real estate markets in the region. 2025 proved that even in a higher-rate environment, this market delivers stability, appreciation, and opportunity.

As we head into 2026, momentum is building—not from hype, but from fundamentals.

If you’re wondering what this market means for your home’s value, a buying strategy, or new construction opportunities, those conversations matter more than ever.

Connect with your trusted Better Homes and Gardens Real Estate Journey agent to talk through what’s next.

If you’ve noticed more new faces at your favorite Bentonville coffee shop or a few extra bikes cruising down the Razorback Greenway, you’re not imagining things — Northwest Arkansas has officially arrived. Once considered one of the South’s best-kept secrets, this region is now a magnet for professionals, families, and creatives who want it all: natural beauty, thriving communities, and homes that actually feel like home.

If you’ve noticed more new faces at your favorite Bentonville coffee shop or a few extra bikes cruising down the Razorback Greenway, you’re not imagining things — Northwest Arkansas has officially arrived. Once considered one of the South’s best-kept secrets, this region is now a magnet for professionals, families, and creatives who want it all: natural beauty, thriving communities, and homes that actually feel like home.